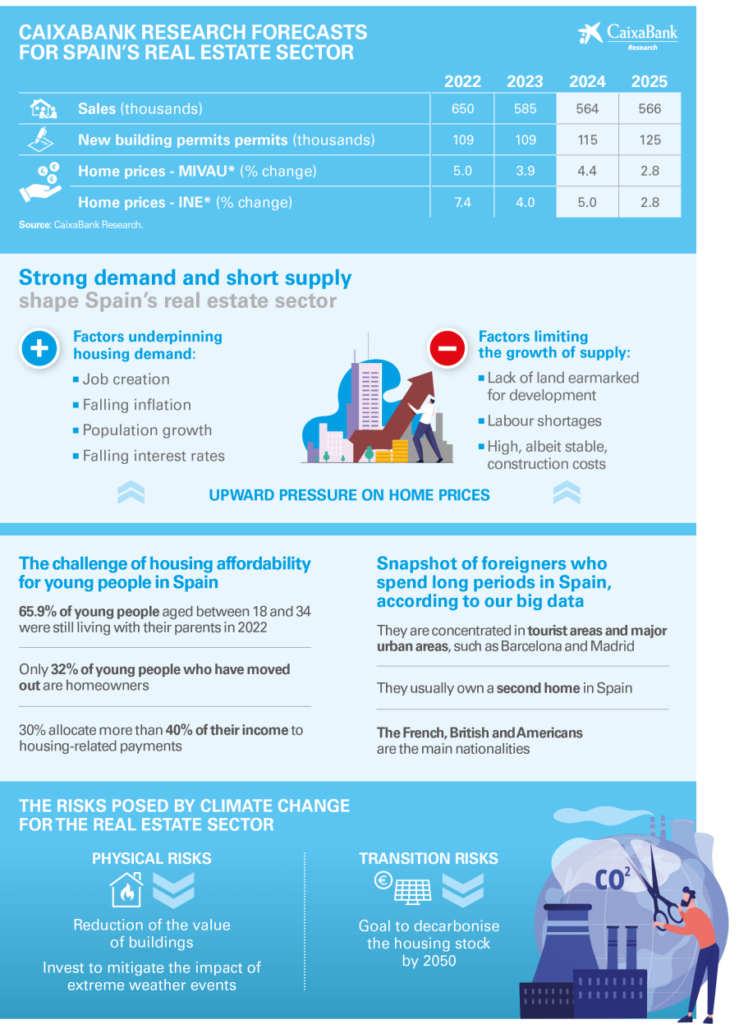

The first half of 2024 has been marked by rapid increases in both demand and prices in Spain’s real estate market, with a somewhat more timid increase in supply. This greater than expected buoyancy has led us to revise upwards our forecasts for Spain’s real estate sector for 2024 and 2025. At CaixaBank Research, we predict that the number of sales will reach around 565,000 units per year and that home prices will rise by around 5.0% in 2024, followed by a slightly more contained growth rate of 2.8% in 2025 (forecasts from the previous Real Estate Sector Report of February 2024: 2.7% and 2.5%, respectively). In the first article of this report we set out this new forecast scenario in greater detail.

The production of new housing will continue to be weighed down by a number of structural factors, such as the lack of land earmarked for development and the shortage of skilled labour, which are holding back the housing supply in a context of high demand. In particular, we expect around 115,000 planning permission applications to be granted in 2024, gradually rising to 125,000 in 2025. These figures fall far short of the new projections just published by the National Statistics Institute for the number of households: 330,000 net households are expected to be created each year in the period 2024-2028, compared to previous projections of around 220,000 households in the same period. In the absence of a significant increase in the housing supply in the coming years, the gap between supply and demand will steadily widen, and this could apply further pressure on home prices, especially in areas that are experiencing more rapid demographic growth.

These dynamics in the housing market are exacerbating the housing affordability problems that are affecting certain groups, such as young people. We analyse this issue in the second article of this report. Solving the affordability issue is no easy task and requires action to be taken on multiple fronts and over an extended time horizon. Public-private collaboration is essential for boosting the supply of affordable housing, and industrialised construction shows promise as a new way to help overcome the major challenges that the sector is facing.

In the third article we carry out an in-depth analysis of foreigners who visit Spain for relatively long periods, using data on payments made with foreign cards recorded on CaixaBank POS terminals. We observe that these visitors are concentrated in the provinces where foreigners tend to buy second homes in Spain, such as Alicante, the Balearic Islands, the Canary Islands and Malaga, although they are also found in the country’s major urban areas such as Barcelona and Madrid.

In the last article of this Sector Report, we focus on the risks that climate change poses to the housing market. These include extreme weather events, referred to as physical risks (floods, forest fires or more gradual changes in the climate, such as sea level rise), which could lead to a significant reduction in the value of buildings. On the other hand, the real estate sector is also being affected by the need to adapt to stricter regulations in order to mitigate and adapt to climate change, collectively referred to as transition risks. The role of public policies is crucial for encouraging the conversion of the housing stock in order to cut greenhouse gas emissions and mitigate the impact of physical risks, especially among the most vulnerable groups in society, in order to ensure an efficient and fair climate transition.